Two years ago, Zoos Industrial Research wrote the "2016 ADAS and Autonomous Driving Industry Chain Report", which was subdivided into three reports, totaling about 500 pages. With the development of the automobile industry and the growth of the autonomous driving industry, when we updated this report this year, we had to substantially expand it to seven reports, totaling about 1,200 pages.

The seven industry chain reports are:

"2018 ADAS and Autonomous Driving Industry Chain Research-Computing Platform and System Architecture"

"2018 ADAS and Autonomous Driving Industry Chain Research-OEMs and System Integrators"

"2018 ADAS and Autonomous Driving Industry Chain Research-Automotive Vision Industry"

"2018 ADAS and Autonomous Driving Industry Chain Research-Automotive Radar Industry"

"2018 ADAS and Autonomous Driving Industry Chain Research-Low Speed ​​Autonomous Driving Industry"

"2018 ADAS and Autonomous Driving Industry Chain Research-Commercial Vehicle Autonomous Driving Industry"

"2018 ADAS and Autonomous Driving Industry Chain Research-Autonomous Driving Startups"

"2018 ADAS and Autonomous Driving Industry Chain Research-Computing Platform and System Architecture" has 158 pages, including seven parts:

Introduction to ADAS and Autonomous Driving

ADAS and Autonomous Driving Market Forecast

ADAS and autonomous driving strategies of domestic automakers, including Geely, GM, SAIC, Dongfeng, Great Wall, GAC, Changan, Weilai, Xiaopeng, Byton and other manufacturers

ADAS and autonomous driving software architecture, including Autosar classic and adaptive, ROS 2.0 and QNX

ADAS and autonomous driving hardware architecture, including vehicle Ethernet, TSN, Ethernet switching and gateway, domain controller

ADAS and autonomous driving safety certification, including ISO26262, AEC-Q100

Research on processor manufacturers, including NXP, Renesas, Texas Instruments, Mobileye, Nvidia, Ambarella, Infineon, ARM, etc.

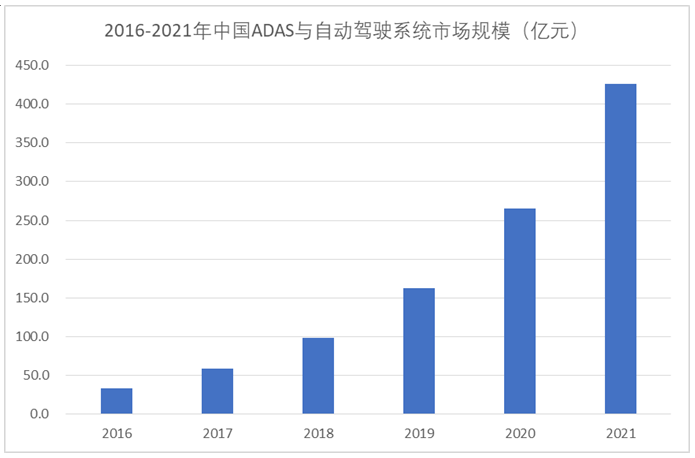

According to research conducted by Zoath Industrial Research, the scale of China's ADAS and autonomous driving market was approximately 5.9 billion yuan in 2017 and is expected to reach 42.6 billion yuan by 2021, with an average annual growth rate of approximately 67%.

The first segment of the market is automotive vision, millimeter-wave radar, and ADAS systems. The scale and growth rate of the millimeter-wave radar market are surprising. Next is low-speed automatic driving, and the market enlargement of lidar, commercial vehicle automatic driving, and passenger car automatic driving will be relatively lagging.

After the automobile enters the era of ADAS and autonomous driving, the product iteration speed has increased rapidly, and the automotive market is far less extensive than the consumer electronics market, but the design difficulty, design and production costs are higher than the consumer electronics market, and the product iteration speed has increased significantly. The product life cycle is shortened, and the risk of automotive ADAS and autonomous driving processors is greatly increased. Sufficient financial and human resources must be available to support the development of automotive ADAS and autonomous driving processors. Only a few companies such as NXP and Renesas can Develop a full range of ADAS and autonomous driving processors.

In terms of safety certification, autonomous driving chips require at least ASIL B level. Currently, only Renesas R-CAR H3 is the only autonomous driving processor that can achieve ASIL B safety certification. GPU is a general-purpose design, not a car-specific design. From the design point of view, it is difficult to achieve the safety level of ISO26262 certification. The ASIL certification cycle is as long as 2-4 years.

The reliability, accuracy, and functionality of the binocular are far better than those of the monocular, but because the binocular must use FPGA, the cost is high. Cost-restricted binoculars can only be used in the field of luxury cars. With the emergence of hardcore binocular processors from Renesas and NXP, binoculars will appear in the fields of ADAS and autonomous driving in large numbers, from luxury cars to mid-range cars.

With the rapid increase in data transmission, in-vehicle Ethernet will become the standard configuration of future cars, and automatic driving will not be possible without Ethernet switches or Ethernet switches.

Autosar will become a standard configuration in the field of ADAS and autonomous driving.

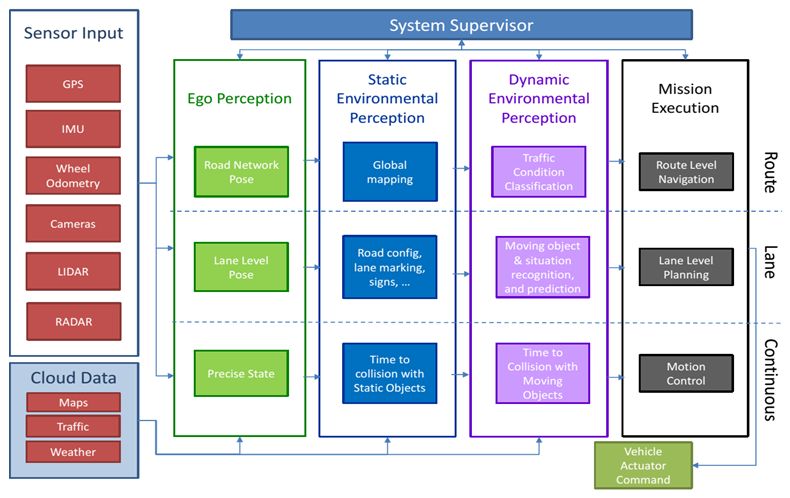

Typical unmanned driving frame

CNN/DNN graphics machine learning, data and order have nothing to do, GPU is the most suitable, especially in terms of cost performance, NVIDIA GPU can be used in many fields other than automobiles, and the shipment volume is much higher than that of automobile-specific ASICs. The price/performance advantage is very obvious. The TPU improves the speed by reducing the calculation accuracy and reduces the power consumption. The power consumption is only 10% of the GPU.

RNN/LSTM/reinforcement learning For sequential machine learning, FPGA has obvious advantages, especially in terms of power consumption. Under the same performance, FPGA is less than 1/5 of GPU. However, FPGAs lack cost performance, and high-performance FPGAs are costly. FPGA can also handle graphics machine learning, which can reduce accuracy to improve performance.

ASIC performance and power consumption ratio is the best, but the development cycle is long, the development cost is the highest, and the flexibility is the worst. If the shipment is low (if the 7-nanometer process is used, the minimum annual shipment is 120 million), or the unit price Very high, or the manufacturer is losing money. Most deep learning graphics machine learning ASICs are similar to TPU.

In the automotive field, power consumption and cost-effectiveness are key factors. For graphics machine learning, GPUs are undoubtedly the winners. However, with the continuous improvement of algorithms, the requirements for operation accuracy are getting lower and lower, and the low power consumption of FPGA makes it also have a place in the field of graphics machine learning. For sequential machine learning, FPGA has an overwhelming advantage.

Autonomous driving can be divided into two types. One is Waymo, which has solved most of the problems in the field of environmental perception. The focus is mainly on behavioral decision-making. The computing architecture is CPU+FPGA, generally Intel Xeon 12 CPU above core plus FPGA of Altera or Xilinx. The other is represented by Mobileye, which has not yet solved all the problems of environment perception. The energy is mainly in environment perception. The computing architecture is CPU+GPU/ASIC.

Looking to the future, CPU+GPU will be the mainstream in the short term, but CPU+FPGA/ASIC may be the mainstream in the long term. The main reason is the improvement of algorithms and the performance of sensors, especially lidar. The accuracy of graphics operations can continue to decrease. This is very beneficial to FPGA, and GPU power consumption is difficult to reduce. FPGAs are easier to meet vehicle-level requirements.

In the field of chip foundry, TSMC has won all 7-nanometer orders, including the exclusive supply of Apple’s A12. This is the first time that TSMC has surpassed Intel to become the most advanced manufacturer of semiconductor manufacturing processes, such as artificial intelligence autonomous driving digital logic chips that emphasize computing capabilities , Advanced technology must be adopted.

Logic Gates And Inverters,Circuit Logic Gates And Inverters,Logic Chip Gates And Inverters,Gates And Inverters Logic Output

Shenzhen Kaixuanye Technology Co., Ltd. , https://www.iconlinekxys.com